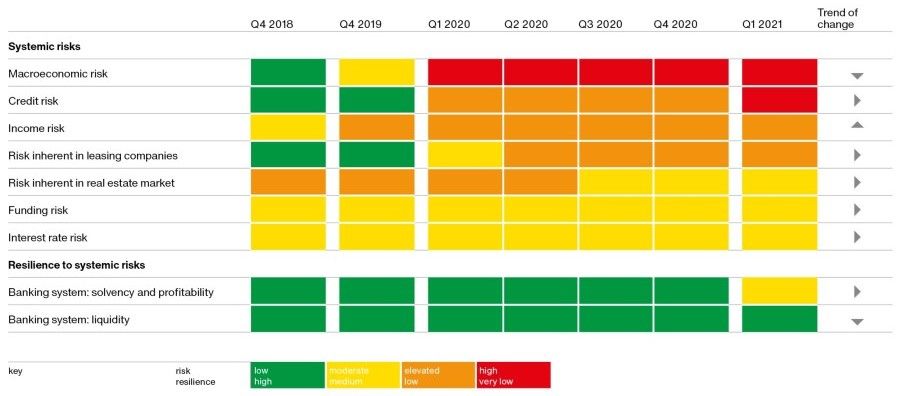

The systemic risks to financial stability remain elevated in the Covid-19 epidemic. Macroeconomic risk remains high, although it is gradually diminishing as businesses and households increasingly make adaptations. Credit risk is becoming more evident with the gradual withdrawal of the extensive government measures to support businesses and households. Income risk remains elevated. The new Financial Stability Review further finds that the financial system’s resilience to systemic risks remains relatively high, given the good position in which it entered the crisis, and the speed and scale of the economic policy measures taken.

Here we particularly note that alongside the current challenges, the banking system is also facing structural changes that demand a clear strategy of action.

Banka Slovenije actions

Under the aegis of the Governing Council of the ECB, we have put extensive monetary policy measures in place to alleviate the crisis. The highlights include the introduction of the pandemic emergency purchase programme (PEPP) with an envelope of EUR 1,850 billion and a horizon to March 2022, with the principal of maturing securities being fully reinvested at least until the end of 2023. In the area of regulatory activities, numerous capital and regulatory reliefs were adopted within the framework of the Single Supervisory Mechanism and the European Banking Authority, making it easier for banks to do business and to provide the requisite support to the real sector.

All the measures applying to the systemically important banks were also applied to the other banks in the Slovenian banking system by Banka Slovenije. The measure freezing dividend payments has been extended and adjusted this year. This is helping to ensure the retention of capital at banks, so that the Slovenian banking system is better able to withstand potential losses, and to continue supplying credit to businesses and households. The regulation on macroprudential restrictions on consumer lending was adjusted so that a temporary decline in a consumer’s income during an official epidemic period can be excluded from the calculation of his/her creditworthiness.

Key risks to the banking system

Amid a recovery in the sectors not under the direct impact of the containment measures, the economic situation remains difficult. Macroeconomic risk consequently remains high, although it began to decline as a result of the improved outlook for emergence from the crisis in the final quarter of 2020.

Credit risk worsened, as the gradual expiry of the extensive government measures to support businesses and households will make the deterioration in the quality of the banking system’s credit portfolio more evident, and this will be reflected in an increase in non-performing exposures. This will bring an end to the period of several years of successful reduction in NPEs, which will begin to rise again. After three years of net release, the banks recorded a net increase in impairments and provisions in 2020.

The conditions for generating income in the banking system worsened further, in the wake of last year’s sharp slowdown in growth in bank lending. Income risk therefore remains elevated, with a trend of increase.

Resilience of banks

The banks’ resilience to systemic risks, which was high for the majority of 2020, has deteriorated in the solvency and profitability segments, and is now medium. Amid the anticipated deterioration in the quality of the credit portfolio, the banks might also begin to see a decline in their capital ratios. There is also considerable variation in the level of resilience at individual banks, given the differences in the structure and quality of their credit portfolios and in their capital surpluses. Bank resilience in the liquidity segment remains high, again with variation between individual banks.

Structural challenges to the banking system

Banka Slovenije notes that the last decade has brought structural changes to the banking system balance sheet. The particularly pronounced changes seen in Slovenia mainly reflect the banks’ shift from corporate lending to household lending, so that the current balance between individual elements of bank balance sheets is out of kilter with the traditional idea of financial intermediation that we are used to. Consequently it will be necessary to find a new consensus with regard to the banking sector’s business strategy in the conditions of the new normal. This deliberation should be set in a broader context, and alongside the usual questions with regard to future demand for banking products, target customer groups, digitalisation, etc., it should also relate to employee competencies at all levels, the search for competitive advantage in the banking market, and an assessment of the ability to secure additional equity to ensure the banks’ successful future development in these conditions. Only such a well-considered strategy can guarantee the long-term viability of the banking system, to ensure that the economy as a whole is properly served.

Publication is available on the link.