The outlook in the euro area improved in March before the renewed tightening of containment measures, although euro area countries are in different starting positions before the anticipated recovery. In Slovenia all sectors not being directly impacted by containment measures are recovering. The figures show signs of moderate, albeit uneven, economic growth in the first quarter of this year. The situation on the labour market remains good, under the influence of the government support measures, but gaps have widened between individual groups of workers. There remains much uncertainty in connection with the future evolution of the epidemic. The Economic and Financial Developments publication makes it clear that non-financial corporations, households and banks entered the crisis in good financial shape, while changes to their behaviour have occurred during the epidemic.

The outlook for global economic growth is improving, despite the major uncertainty in connection with the pandemic. Compared with certain other major global economies, the euro area is not in the best position before the anticipated improvement. Its recovery is dragging, and it is also facing a vaccine shortage and large economic gaps between different countries. The outlook nevertheless improved in March, before the renewed tightening of containment measures.

All sectors of the domestic economy not under the direct impact of the containment measures are recovering. Evidence that firms are significantly adapting to the difficult situation comes from the decline in the share of badly hit sectors. Sectors that were suffering a decline in value-added in the final quarter of last year, when the epidemic was at its peak, accounted for 31% of GDP (compared with 76% during the spring outbreak of the epidemic).

Some signs of moderate, albeit uneven, economic growth had also appeared by the first quarter of this year. Industrial production is strengthening as foreign demand rises, while construction is recovering in parallel with investment. There is also great potential for growth in private consumption: household savings are high, and consumer propensity to spend was evidenced in a sharp increase in total card payments. The renewed tightening of containment measures in the first half of April brought the recovery in certain service sectors to a temporary end, or further delayed the recovery in those sectors yet to see one. The outlook for the second quarter of this year is nevertheless good, at least judging by the survey figures for demand expectations.

February’s partial lifting of the containment measures was also reflected on the labour market, although uncertainty remains great as the epidemic persists. Registered unemployment stood at 81,616 in early April, up just 4,132 on the beginning of the epidemic. The number of notified vacancies rose, as did firms’ employment expectations. Support from the emergency measures will remain the key to preventing a downturn; most notably the furlough scheme has prevented a much sharper fall in employment.

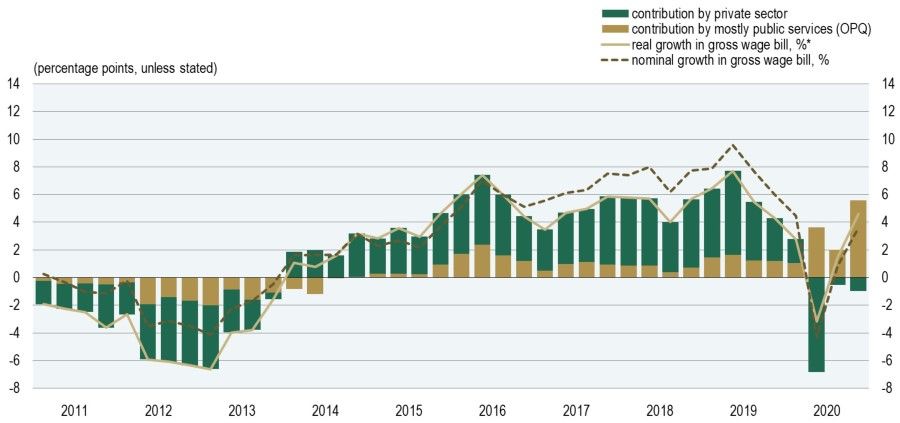

While labour market indicators remain stable on aggregate, the gaps between different groups of workers have widened. Employment fell sharply in trade and in accommodation and food service activities, particularly in the second wave of the epidemic: the year-on-year fall stood at 15.0% in January of this year, in contrast to the rise in employment of 5.0% in human health and social work activities amid the increased demand for staff. There are also pronounced differences in wage growth. Growth in the average gross wage in mostly public services is strongly outpacing growth in the private sector, amid high payments in connection with the epidemic. The average wage in human health and social work activities was up 41.9% in year-on-year terms in January, while in the private sector it was up 3.2% following a rise in the minimum wage.

Figure 1: Year-on-year growth in the gross wage bill according to national accounts

Sources: SORS (national accounts), Eurostat, Banka Slovenije calculations

Amid the strengthening of certain foreign and also domestic inflationary pressures, Slovenia emerged from deflation in March (with annual inflation of 0.1%, up 1.2 percentage points on the previous month), but price developments remained weak. As expected, rising energy prices were the key factor.

Last year’s general government deficit was large as expected, and reached 8.4% of GDP. General government revenues declined by 4.6%, most notably as a result of a fall in indirect taxes driven by the shock in private consumption, and a fall in direct taxes driven by corporate income tax. The position was further hit by a rise of 14.8% in expenditure; according to current estimates, the measures to alleviate the epidemic were among the largest in the euro area as a share of GDP. The general government debt had reached 80.8% of GDP by the end of last year, up approximately 15 percentage points on a year earlier, but still significantly less than the euro area average. Borrowing remained heavy in the first quarter of this year, amid the favourable terms driven by monetary policy measures and good credit ratings. Slovenia’s sovereign borrowing costs on the capital markets have declined to a very low level: the yield on 10-year government bonds is now 0.02%. The spread over the German benchmark also declined to a record low (approximately 30 basis points).

As a result of the crisis, the gross external debt increased sharply last year (by EUR 4.4 billion to EUR 48.2 billion, or 104.1% of GDP), driven largely by government borrowing; in contrast to the position before the outbreak of the previous crisis, government debt accounts for fully half of the total external debt.

Banka Slovenije further finds that non-financial corporations, households and banks entered last year’s crisis in a good financial position, but the financial accounts reveal significant changes in their behaviour in 2020. As a result of the introduction of the emergency measures and the corresponding sharp increase in borrowing at the outbreak of the epidemic, the largest reversal came in the government sector. After two years of net saving, its negative net financial position deepened sharply last year. By contrast, from the outbreak of the epidemic other sectors further strengthened their saving relative to investment, particularly non-financial corporations and households. Their excess saving flowed in the form of deposits to banks, who in turn continued to place the money with the central bank. The year-on-year increase in the banks’ financial assets and liabilities last year underwent its most pronounced surge of the last ten years.

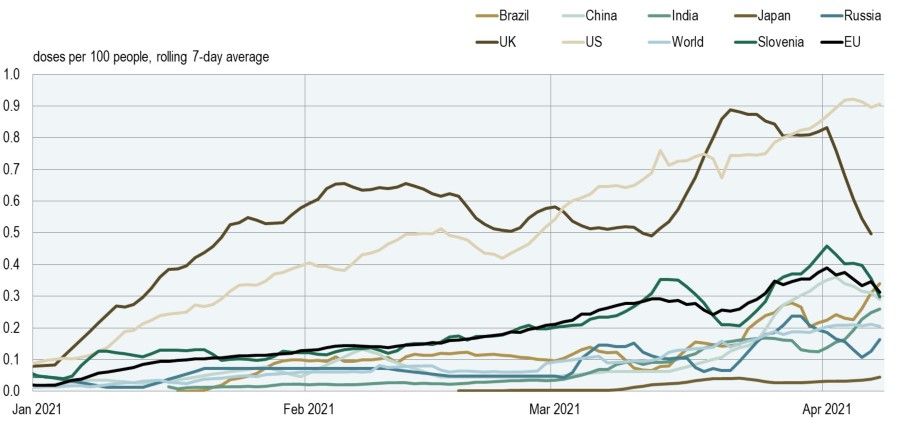

Figure 2: Daily vaccine doses administered*

Note: *Individual doses are shown, and may not correspond to the total number of people vaccinated, depending on the specific dose regime for each vaccine.

Source: Our World in Data

Publication is available on the link.