There were hints of an improvement in the global economy in the final quarter of last year, while signs could also be seen of the uncertainty in international trade easing. Indicators of economic activity in the euro area remained sluggish, and growth in the Slovenian economy is also thought to have slowed slightly, according to the figures currently available. However, the labour market remains sound in Slovenia and in the euro area, even though economic indicators are weak. Inflation remains moderate, despite strengthening cost pressures at firms. These are the key findings of the latest issue of the Bank of Slovenia’s Economic and Financial Developments publication, which was released today by the Bank of Slovenia, and which also highlights the increased uncertainty in which the planning and administration of fiscal policy are undertaken.

Signs of an improvement in the global economy could be seen at the end of last year, and the uncertainties in international trade might be reduced by the signing of a trade agreement between China and the US. In the euro area the PMI and confidence indicators in the final quarter of last year were down on the third quarter on average, but picked up again slightly at the end of the year. Wage growth and employment growth remain solid, particularly compared with the weak indicators of economic activity.

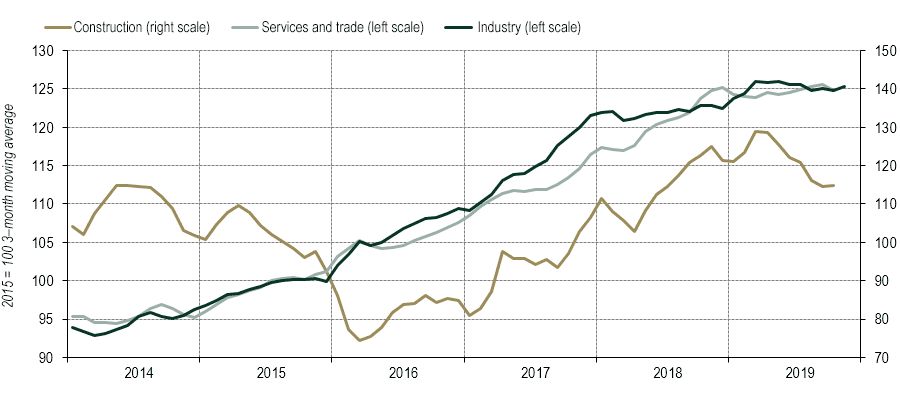

Economic growth in Slovenia slowed again in the final quarter, according to the available monthly indicators. Year-on-year growth in industrial activity was barely above 1% in November, and for the most part was based merely on increased output in the automotive and pharmaceutical industries. The weak growth in foreign demand is increasingly being reflected in real turnover in private-sector services, which in October was actually down on a year earlier. At the same time the end of the investment cycle in local government meant that construction activity remained weak. The economic sentiment declined again in the final quarter of last year, but a slightly more encouraging picture is being painted by the indicators of foreign demand, which have begun to stabilise. This is being suggested by a survey of manufacturing by the SORS, and the latest forecasts for this year’s economic growth in Slovenia’s trading partners.

Figure 1: Monthly economic activity indicators

Sources: SORS, Bank of Slovenia calculations

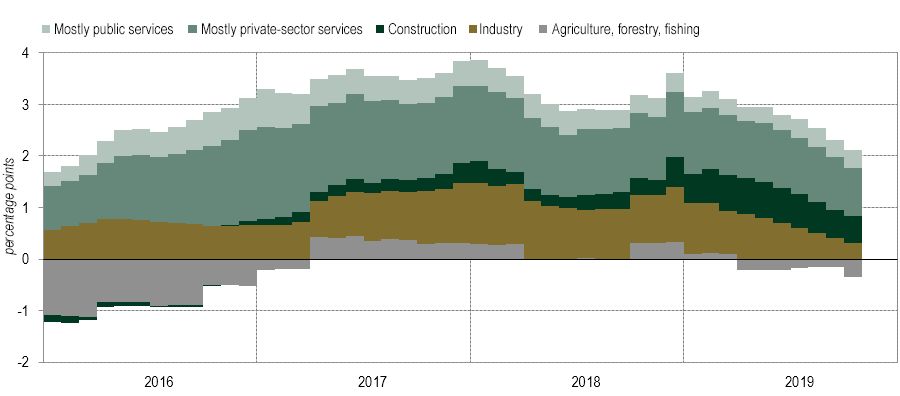

Similarly to the euro area, in Slovenia too the situation on the labour market remains relatively good, given the slowdown in the international environment and in the domestic output climate. Employment growth is slowing, but remains high relative to GDP growth. Labour costs are continuing to rise, and nominal growth in the average gross wage over the first ten months of last year was almost 1 percentage point higher on average than in the previous year. Because labour productivity is stagnating at the same time, cost pressures are strengthening, which is being reflected in higher core inflation (headline inflation remains moderate, having averaged 1.7% in 2019), and a weakened dynamic in certain competitiveness indicators. The same process is driving higher growth in private consumption.

Figure 2: Contributions to year-on-year change in the workforce in employment

Sources: SORS, Bank of Slovenia calculations

The current account surplus exceeded EUR 3.0 billion over the 12 months to November, the highest figure to date according to the current balance of payments data. The main reason was the ongoing increase in the surplus of trade in services, despite a sharp slowdown in exports in the second half of the year. The declining growth in foreign demand saw growth in merchandise exports slow sharply – exports in November were actually down in year-on-year terms – but weak investment and low growth in industrial production brought an even sharper slowdown in growth in imports of capital goods and intermediate goods.

Despite the weaker economy, the general government position remains in surplus. The relatively high 5.9% growth in revenues was partly attributable to the still-buoyant labour market, and higher capital income, while the tax break on annual leave allowance had a negative impact on revenues. Borrowing terms on the international financial markets are good at present. Planning and administering fiscal policy requires particular caution, as there remain considerable uncertainties in international trade, while the domestic economic indicators were also slightly weaker in the final quarter of last year.

Publication is available here.