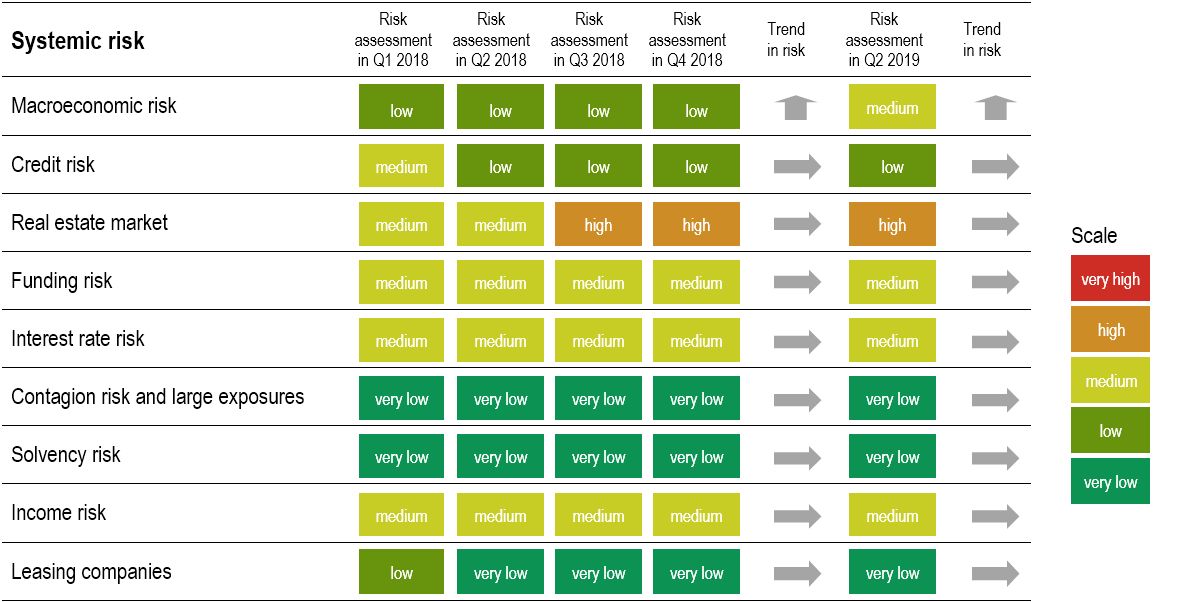

The financial system in Slovenia remained stable last year and in the first quarter of this year, but the risks to stability are increasing. The risks inherent in the real estate market remain elevated, as prices of residential real estate have been rising fast for some time now. There was also a significant increase in macroeconomic risks, primarily as a result of a slowdown in global economic growth and increased uncertainty in the international environment. In the wake of the anticipated slowdown in the economy, the key challenge for the banking system will be generating stable income in a situation of low interest rates. This is vital to maintaining the resilience of the banking system, particularly in the event of a significant deterioration in the situation. These are the key findings of the Financial Stability Review, which also examines the Bank of Slovenia’s macroprudential instruments used to increase the resilience of the banks and to mitigate systemic risks.

The Bank of Slovenia finds that the banking system in Slovenia remains robust. Although assessed as moderate, macroeconomic risks have increased, primarily as a result of uncertainties in the international environment. The elevated risks inherent in the real estate market are also highlighted, with residential real estate having seen fast-rising prices for some time now. This was primarily attributable to an imbalance between supply and demand on the market, although growth in housing loans remains moderate.

Bank of Slovenia measures

The Bank of Slovenia is also using macroprudential policies to enhance the robustness of the banking system to the increased risks, and has adopted six measures to date. Given the risks identified, there is an emphasis on the banks’ need to meet the macroprudential recommendation for the maximum level of housing loans that they may approve relative to the collateral and the borrower’s income. The proportion of banks failing to meet the recommendation is found to be high, but stable. Last year the recommendation was extended to consumer loans, in light of their rapid growth. They represent a potential source of increased credit risk in the future. Credit risk has been diminishing in recent years, but remains significant in the corporate segment.

Generating stable income while interest rates remain low will be a challenge for the banking system in the future. The banking system was highly profitable in 2018, although the net interest margin and growth in net interest income were low. There was a net release of impairments and provisions for the second consecutive year. Hypothetically, had the ratio of impairment and provisioning costs to gross income been at its long-term average, pre-tax profit in 2018 would have amounted to less than a third of the observed figure.

In the low interest rate environment, which sharply reduces the room for further cuts in interest expenses, the banks’ profitability is highly dependent on the scale of lending activity. This increased in 2018, and focused primarily on household loans, but in the event of a slowdown in the economy it could begin declining again, thereby slowing growth in net interest income and bank profitability.

Meanwhile corporate lending remains weak. Corporate financing at banks is modest, despite the favourable borrowing terms, relatively low corporate indebtedness, and the improvement in creditworthiness relative to previous years. Firms have more internal resources, and the proportion of financing obtained in the rest of the world has increased, while the structure of the corporate sector has also changed.

High bank liquidity means that funding risk remains low, but is increasing as the maturity gap between assets and liabilities widens. The maturity of new loans is lengthening, while the maturity of deposits is shortening. This is also being addressed by a macroprudential measure, which recommends that banks maintain a ratio of at least one between total financial assets and total funding with a residual maturity of up to 30 days.

Systemic insolvency risk also remains low: the banking system was well-capitalised in 2018, although there were major differences in the capital position from bank to bank.

Structural risks

An unambiguous rising trend is also evident in the risks inherent in climate change. These are long-lasting structural changes, which are bringing numerous known and unknown risks into the financial system. In part these risks come from the direct exposure of the financial system and its clients to climate change, while further risks are brought by the urgency of the transition to a low-carbon economy and society. The growing risks related to digitalisation have a similar non-cyclical, structural nature; the most significant of these are cyber risk and critical (financial) infrastructure risk.

Figure: Overview of risks in the Slovenian banking system

Source: Bank of Slovenia

Publication is available here.